Launch

Launching a Functional Drink in DACH: A 90-Day Market-Entry Playbook

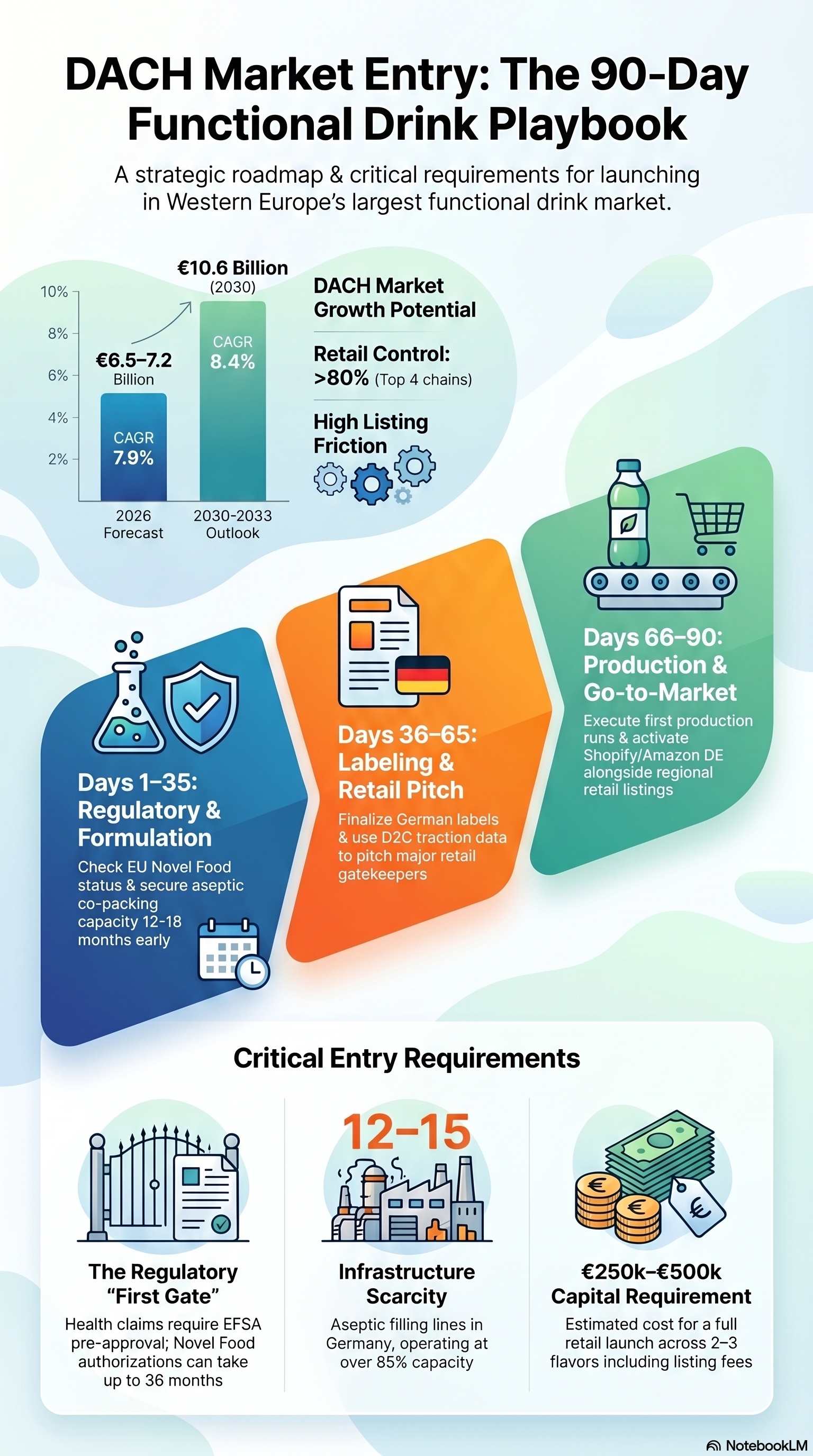

Why the DACH Market Rewards Prepared Newcomers

The German functional drinks market is projected to reach US$ 10,685 million in revenue by 2030, growing at 8.4% annually from 2025 (Grand View Research). This growth concentrates in segments that barely existed five years ago: nootropics for cognitive performance, gut-health beverages, beauty-from-within formulations, and hybrid performance drinks. The market has shifted from basic energy drinks toward targeted functional benefits. Brands with a single clear benefit proposition — sleep, focus, immunity — achieve 2–3x higher trial rates than "all-in-one" formulations.

What makes DACH unique is not just the market size — Germany alone accounts for approximately 4.4% of global functional drink revenue — but the combination of regulatory stringency, high consumer standards, and a retail structure dominated by a few gatekeepers. EDEKA, Rewe, Lidl and Aldi jointly control over 80% of grocery sales (IndexBox 2026). Listing fees for a single SKU at a national chain run between €5,000 and €25,000, and prerequisites include IFS or BRC certification, clean-label compliance, and proven D2C traction data.

Phase 1: Regulatory Audit — Day 1–15

Regulatory classification is the single most common reason functional drink launches stall. Any ingredient not consumed to a significant degree within the EU before 15 May 1997 requires a Novel Food authorisation under Regulation (EU) 2015/2283 — a process lasting 18–36 months (EFSA procedural guidance, 2025 update). Adaptogens such as ashwagandha, rhodiola and hemp-derived cannabinoids fall into this category; many botanical extracts sit in the grey zone of the EU Novel Food catalogue and require a formal determination from the competent authority of the member state.

For established ingredients, the next hurdle is the EU Register of nutrition and health claims (Regulation EC 1924/2006). Only pre-approved claims by EFSA may appear on packaging or in marketing. The BfR (Federal Institute for Risk Assessment) sets recommended maximum levels for vitamins and minerals, and the BVL (Federal Office of Consumer Protection and Food Safety) enforces strict interpretation of botanical claims. The sugar tax (reformed 2023) levies €0.32/litre on drinks with >8 g sugar/100 ml and €0.16/litre on >5 g/100 ml, which has driven a 20–30% sugar reduction across the category since 2021.

Phase 2: Formulation & Co-Packer Contract — Day 16–35

Germany has 12–15 high-volume aseptic filling lines servicing the RTD beverage co-packing market, with utilisation rates above 85%. Lead times for new functional drink lines run 12–18 months. Key co-packers include Elb-Milch (aseptic rPET filling, 3 lines, 12-month shelf life), Krüger Group (dairy, water and plant-based RTDs), Dico Drinks (cans, full-service development), Peter Mertes KG (multi-format, IFS/BRC certified), and Pomona Bottling (glass and aluminium, up to 55,000 bottles/hour).

Functional ingredients — probiotics, enzymes, natural colourants, heat-sensitive vitamins — often require cold-chain logistics throughout the supply chain. Only an estimated 60–65% of German beverage distributors have cold storage capacity (IndexBox 2026). Co-packers offering in-house stability testing, accelerated shelf-life trials, and micro-encapsulation command 20–30% premium pricing but significantly reduce scale-up risk. Minimum order quantities for aseptic PET lines typically start at 50,000–100,000 units per SKU.

Phase 3: Health Claims & Labelling — Day 36–50

Labelling under EU Food Information to Consumers Regulation 1169/2011 must include: ingredients in descending weight order, allergens highlighted, nutrition declaration per 100 ml, and a full INCI listing. German retail increasingly enforces Nutri-Score, penalising high-sugar functional drinks. The EU Green Claims Directive, fully phased in by 2026, requires scientific substantiation for any sustainability claim on pack.

For the German market, labelling must be in German. Switzerland requires trilingual labelling (German, French, Italian). Austria accepts German-language labelling with an Austrian distributor contact. Organic certification (EU Organic Seal) is effectively a prerequisite for premium pricing — 65–75% of functional beverages in Germany carry organic certification (IndexBox 2026). Certification costs range €5,000–€15,000 per product with a 6–12 month lead time.

Phase 4: Retail Listing Applications — Day 51–65

DACH retail listing is the highest-friction step. EDEKA operates a decentralised buying model: approximately 3,500 independent merchants decide their assortment while seven regional companies manage distribution. The foodstarter platform allows suppliers to pitch products directly. Rewe introduced a centralised Start-up Lounge in November 2025 — products receive 3 months of prominent placement in participating Rewe stores.

dm and Rossmann are critical channels for health-oriented functional drinks, posting 5–6% listing growth. Discounters Aldi and Lidl have been expanding private-label functional drink lines at 4–5% per year. Online retail and D2C channels are the fastest-growing at 10–12% per year, particularly for nootropic and specialised functional drinks (Transpire Insight 2026).

Phase 5: Production & Inventory — Day 66–80

With co-packer contracts finalised and packaging materials ordered, the first production run can be scheduled. For an initial launch of 2–3 SKUs (flavours), 100,000–150,000 units per SKU is typical. Per-unit costs for aseptic rPET filling range from €0.45–€0.80. Packaging must comply with the German deposit system: single-use PET bottles >0.1 litres carry a €0.25 deposit (Pfand) and require registration in the LUCID portal.

Quality assurance protocols should include: microbiological testing per EC 2073/2005, stability testing at 25°C/60% RH and 40°C/75% RH across 4 weeks, nutritional analysis, and sensory evaluation. Budget €3,000–€8,000 per formulation run for third-party lab testing of novel or sensitive ingredients.

Phase 6: Go-to-Market — Day 81–90

The go-to-market phase runs on three parallel tracks. First: D2C launch via Shopify or similar e-commerce platforms, supplemented by Amazon DE and online pharmacies. Customer acquisition costs run €8–€15 per first purchase, with a 25–35% repurchase rate within 60 days as the key indicator of product-market fit. Second: retail activation following listing confirmation from regional EDEKA merchants or the Rewe Start-up Lounge. Third: regulatory compliance — for beverages classified as foods rather than supplements, no market authorisation is required, but product safety remains the legal responsibility of the manufacturer.

FAQ

Do I need a Novel Food authorisation for my functional ingredient? Check the EU Novel Food catalogue. If your ingredient was not consumed to a significant degree in the EU before 15 May 1997, authorisation under Regulation (EU) 2015/2283 is required. The process takes 18–36 months.

Can I put "probiotic" or "good for gut health" on my label? The term "probiotic" is not legally defined in EU food law. Health claims require EFSA authorisation under Regulation EC 1924/2006. Most German-market brands use descriptive language such as "with live cultures" instead.

What certifications do I need for EDEKA or Rewe? IFS Food Standard or BRC Global Standard is mandatory for branded suppliers. Organic certification (EU Organic Seal) is expected for premium positioning — 65–75% of functional beverages in Germany carry organic certification.

What does it cost to launch a functional drink in Germany? A conservative estimate for a 2–3 SKU launch including regulatory, formulation, co-packing, certification, packaging, listing fees and marketing is €250,000–€500,000. A D2C-only pathway reduces this to approximately €80,000–€150,000.

How does the sugar tax affect my formulation? Drinks with >8 g sugar/100 ml are taxed at €0.32/litre. Successful 2025–2026 launches target <5 g/100 ml using stevia, allulose or monk fruit as sweeteners.

Sources

- Grand View Research — Germany Functional Drinks Market Size & Outlook 2030

- Sourceready — Germany Functional Beverages Market Report 2026

- IndexBox — Sport & Energy Drinks Market in Germany 2026

- EUR-Lex — Regulation (EU) 2015/2283 on novel foods

- BfR — Questions and Answers on Food Supplements

- EDEKA — EARLY Sparkling Vitamin Drink Launch, March 2026

- EUR-Lex — Implementing Regulation (EU) 2017/2470 (Novel Foods Union List)

- Valoq — How to Succeed in Food Retail DACH

- Transpire Insight — Germany Functional Drinks Market Size 2026–2033

- Market Research Future — Germany Functional Beverages Market 2025–2035

- EFSA — Novel Food Application Procedure

- Bonafide Research — Germany Functional Beverage Market Overview 2030